Refinancing a mortgage to save money was a no brainer when the the brand new breakeven point is actually lower than one year. Recasting home financing to save cash can be beneficial too if your lender lets. I wish to examine the 2 right here.

I have refinanced multiple assets mortgage loans many times once the 2003. However,, You will find never recast a mortgage. This is because since these my loan providers didn’t bring recasting. Nevertheless the large need is simply because I always wished to bring advantage of all the way down home loan pricing.

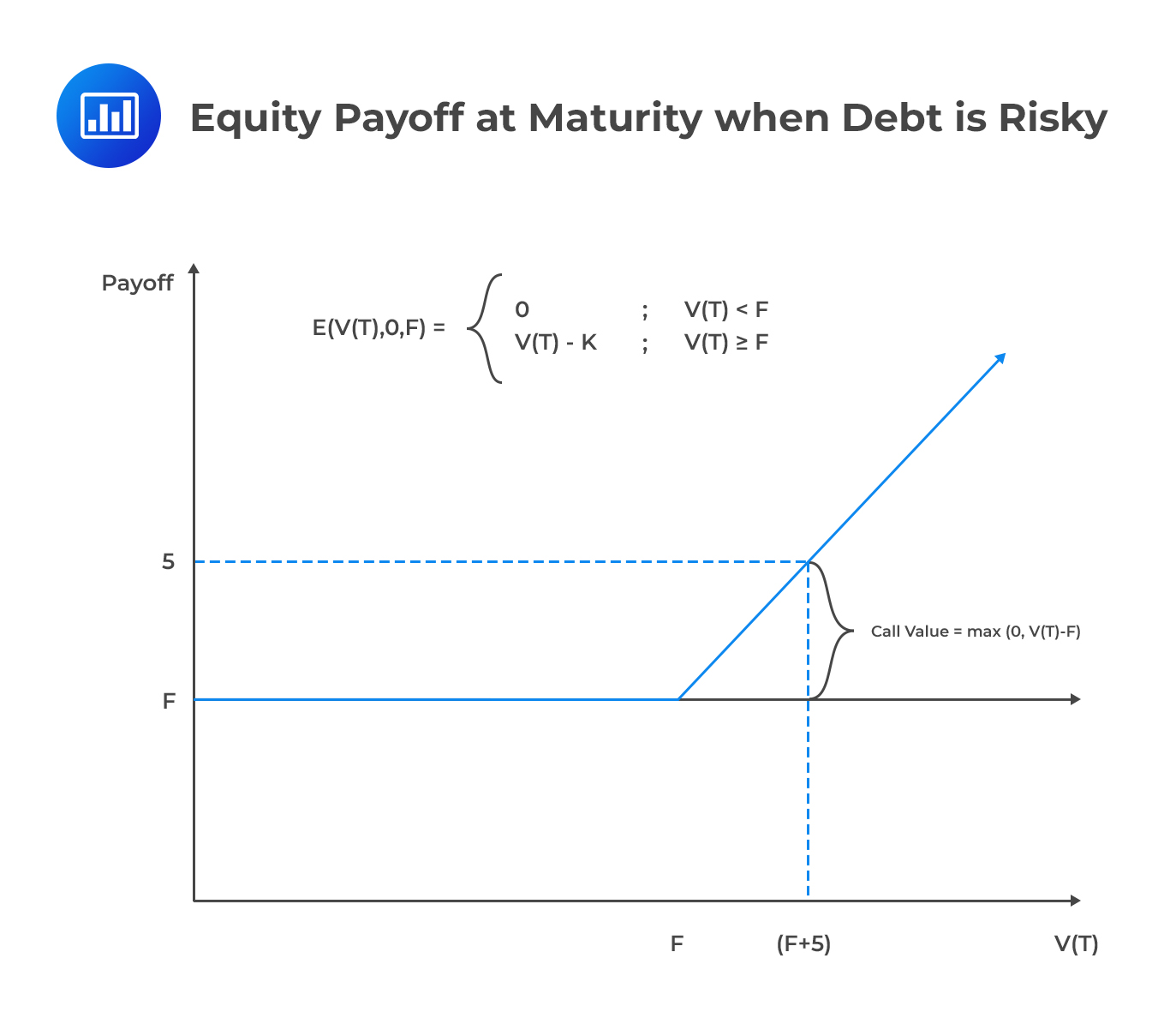

Recasting Instead of Refinancing

Recasting an interest rate will be best for individuals who come into a lump sum payment of money and would like to get rid of your month-to-month homeloan payment while also becoming self-disciplined with paying down their mortgage in line with the modern schedule. After that recasting the mortgage loan makes you prevent the costs so you’re able to re-finance.

However, in my opinion, in terms of recasting in the place of refinancing, it is usually best to refinance. Refinancing a mortgage is usually finest considering the after the grounds:

- Lower interest

- Flexibility

- Exchangeability

Home mortgage Recast Reason

To help help you decide ranging from recasting as opposed to refinancing, allow me to explain exactly what an excellent recast really is. A mortgage loan recast means you are taking a lump sum payment out of bucks and you will lower the principal. If you are the interest as well as your mortgage name will still be unchanged, the month-to-month mortgage payment was reduced to reflect your actual current financing equilibrium.

If you prefer to save something basic provides straight down monthly installments, installment loan Cleveland a mortgage loan recast are a good idea.

Including, if you find yourself five years toward a 30-12 months mortgage, when you recast your loan, you will still keeps twenty five years leftover to expend it well. Whereas, after you refinance a home loan, your amortization plan resets returning to 0. You will have to up coming spend second three decades settling the loan if not shell out a lot more dominant.

Getting recasting to be effective, lenders always need an additional lump sum payment to attenuate the dominating harmony. The greater the additional principal pay down, more you can save with financing.

Alternatively, you could reduce a lump sum payment on your own existing financial rather than recast. However, your own complete month-to-month mortgage repayment matter will not transform.

The single thing you to changes is the percentage mixture of the new fee that happens towards the prominent and you will desire. The greater you pay off, the greater number of the percentage of the percentage would go to principal.

In the event your financial allows you to recast your loan, you should build a lump sum payment to allow having a recast to take place. Usually, the new lump sum was a share of your mortgage equilibrium age.g. 10%, 15%, or 20%. Put another way, the lending company wants to get a hold of a debtor convey more epidermis into the the online game.

Recasting Instead of Simply Paying Principal

Less than try an amortization dining table and this highlights the new description anywhere between principal reduced and you can interest repaid predicated on an effective $700,711 mortgage at the mortgage loan off dos.625%.

See the way the dominant reduced portion rises while the monthly and you will yearly mortgage payment amount of $dos,814 and you can $33,773 stays a similar.

For individuals who pay only down dominating and don’t recast, your own homeloan payment will remain the same at $dos,814 thirty day period. It’s simply new section you to would go to prominent grows.

What is actually Involved in Mortgage loan Recasting?

Home financing recast is a feature in a number of types of mortgages where in actuality the kept payments is recalculated considering a unique amortization plan. During the a home loan recasting, one pays a giant share on its dominant, as well as their home loan is then recalculated in accordance with the this new balance.